")

Medios AG And German Pharma Distribution Industry (OTCMKTS:MEDOF)

Solskin

Investment Thesis

Demand for healthcare is relatively inelastic, which means that in case of a recession, Medios AG (OTCPK:MEDOF) is poised to meet expected growth. Additionally, we believe that the market has already priced in the regulatory risks associated with the company, limiting the downside.

Company Website

The Company

Medios and its subsidiaries are involved in the distribution of specialty pharmaceutical drugs within Germany. The company operates through two segments: Pharmaceutical Supply (85% Revenue) and Patient-Specific Therapies (15% Revenue). Within the Pharmaceutical Supply segment, the company provides products that address various medical conditions, including oncology, neurology, autoimmunology, ophthalmology, infectiology, and hemophilia. The Patient-Specific Therapies segment produces medications tailored to individual patients on behalf of pharmacies, and also offers therapies with individually dosed tablets.

Medios, through strategic acquisitions, has successfully established a robust nationwide network of partners and bolstered its position as a regional leader in real-time supply through its own compounding facilities.

The Industry

In Germany, there are four different categories of drugs for distribution:

-

General sales list medicines (Over-the-counter medicines: OTC), which do not need to be sold in pharmacies.

-

Medicines that can be sold by pharmacists only (apothekenpflichtig).

-

Prescription drugs (verschreibungspflichtig), which are available under a doctor’s prescription only.

-

Narcotic drugs (Betäubungsmittel), which are available under a special narcotic prescription only.

The cost of drugs is covered by either statutory or private health insurance, and pricing is strictly regulated based on factors such as patent protection, finished versus compounded formulations, and whether the drug is patent-protected or off-patent.

The pharmaceutical wholesaler acts as the intermediary between the drug manufacturer and the pharmacy.

Company Investor Presentation

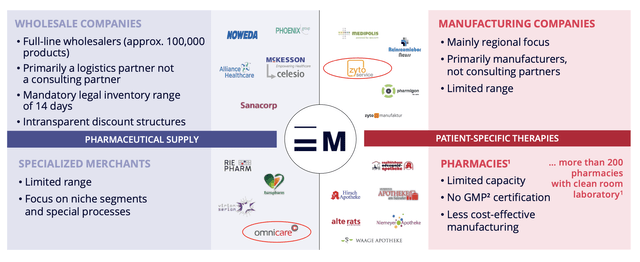

Pharmaceutical Supply

- The wholesale moves the finished product.

- Low margin segment (1-3% EBITDA margin). Margins can increase only thanks to economies of scale.

- Prices are regulated through the German Drug Price Ordinance “Arzneimittelpreisverordnung”.

In this segment, there are two type of companies:

Wholesale companies: typical box mover business model – large quantity – price regulated through ‘Lauer – Taxe’ Specialized Merchants: distribution of only specialized drugs – niche products that require specific expertise – price regulated through ‘Hilfstaxe’.

Specialist wholesalers have a stronger market reach and better placement power than generalist wholesalers due to their close relationship with pharmacists. This allows them to negotiate prices more effectively and cater to specific medical fields and indications. Unlike generalist wholesalers, specialist wholesalers possess the necessary monitoring and compliance structures required to operate within their specialized segment. Generalist wholesalers, on the other hand, excel in efficiently distributing finished medical products across a variety of fields and indications.

Patient-Specific Therapies

- Specialized compounding players.

- Comprises the manufacture of medication on behalf of pharmacies.

- EBITDA margin up to 12% depending on quantity, type of product and distance between distribution center and pharmacy.

Specialty Pharmaceuticals are medications that are designed for rare and/or chronic conditions and are often expensive. Many of these medications are personalized and newly developed, such as infusions that are formulated based on individual disease patterns, body weight, and body surface area. The demand for these therapies is increasing due to their effectiveness. The production of patient-specific treatments requires a high level of expertise, and these specialized medications will continue to have a significant impact on the future of the healthcare system.

Company’s presentation

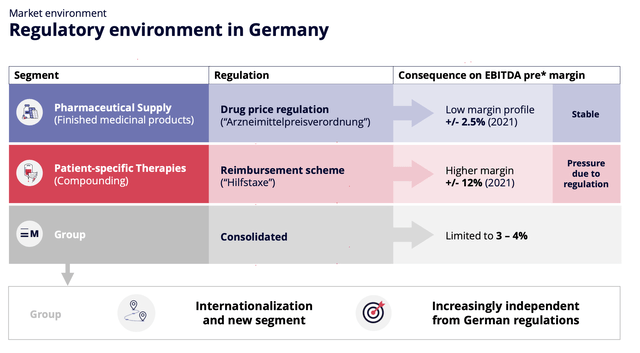

Regulation

Price regulation has had a direct impact on Medios AG, significantly affecting its financial performance and market dynamics.

At the end of August, the arbitration board set the discounts for the active substances Bortezomib, Cabazitaxel and the drugs with the active ingredients bevacizumab, rituximab and trastuzumab. This had an impact on Medios AG pricing. According to the company’s projections, the reduced purchase prices from September 1, 2022, and the adjusted manufacturing prices for the compounding of patient-specific therapies from October 17, 2022, led to a reduction in EBITDA of approximately €3.2 – 3.6 million in 2022.

The share price lost circa 29% since the news.

Medios’s share price (Google Finance)

The issue of regulated prices in generic drugs is a controversial and complex topic that has been debated for many years. On the one hand, regulated prices can provide affordable access to life-saving drugs for patients, particularly in developing countries where healthcare costs are a significant burden. On the other hand, these prices can also have negative consequences for pharmaceutical companies that produce these drugs, potentially leading them out of business.

One of the primary arguments against regulated prices is that it can significantly reduce the profitability of pharmaceutical companies, particularly those that rely heavily on sales of generic drugs. When prices are regulated, companies may not be able to generate sufficient revenue to cover the cost of research and development, manufacturing, and marketing, leading to a decline in profitability.

In the last six months, companies were forced to halt production of certain drugs or exit the market altogether, which had serious consequences for patients who depend on these drugs.

For this reason, Germany and other European countries may need to increase the remuneration for the producers while keeping the final price low to avoid shortage.

The revision of the Pharmaceutical legislation will be discussed by the Parliament and the Council. The discussions will start as soon as possible, but they cannot predict the timing.

The Outlook

Specialty Pharma drugs are driving the transformative market development in Germany, while the landscape of generic distribution is undergoing gradual changes.

Only 5% of the pharmacies are highly specialized pharmacies, despite the huge increase in demand.

Specialty pharma plays a crucial role in addressing and managing chronic diseases. The aging population has led to a significant surge in chronic diseases, resulting in a growing prevalence of such conditions.

In 2022, the Europe specialty generics market was valued at US$ 18.3 billion. IMARC Group projects that the market will grow at a compound annual growth rate (CAGR) of 8.76% from 2023-2028 and reach a market size of US$ 30.5 billion by 2028. This is almost in line with Medios’ organic growth of +7% in 2022.

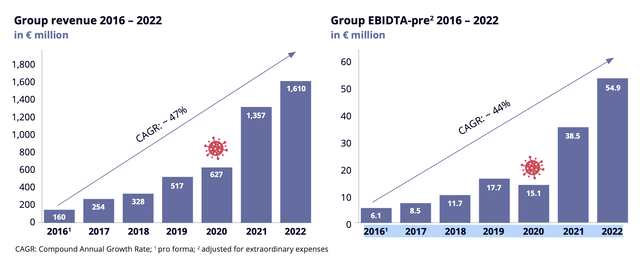

The company grew revenue at a CAGR of 47% in the last 7 years thanks to acquisitions in the Specialty Pharma (Cranach Pharma) and compounding pharma (NewCo Pharma).

Company Investor Presentation

Capacity is now 600,000 (thanks to the acquisitions) and they plan to compound 400,000 products in 2023 from currently 330,000. Assuming that the segment will grow at the same pace as the industry (8.5%), Medios has the ability to meet the anticipated growth in the segment.

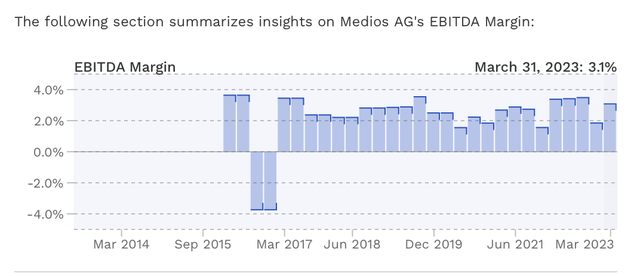

Profitability

EBITDA margin (FinBox)

The company target is to increase EBITDA margin to mid-single digit thanks to the patient-specific segment growth and thanks to the synergies of acquisitions.

The company is reporting EBITDA without extraordinary expenses: adjusted for extraordinary expenses for stock options and M&A activities.

SBC was around 0.2% of revenue in 2022 and averaged 0.3% in the last five years.

Valuation

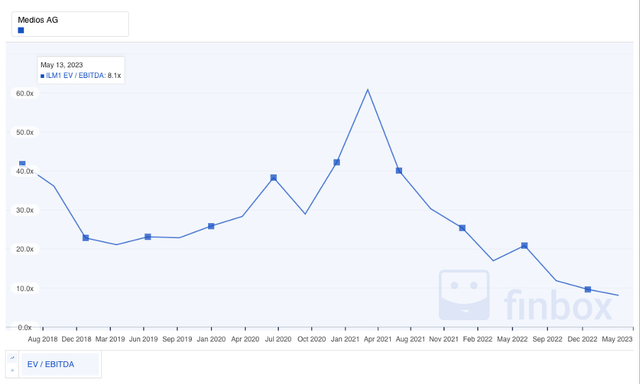

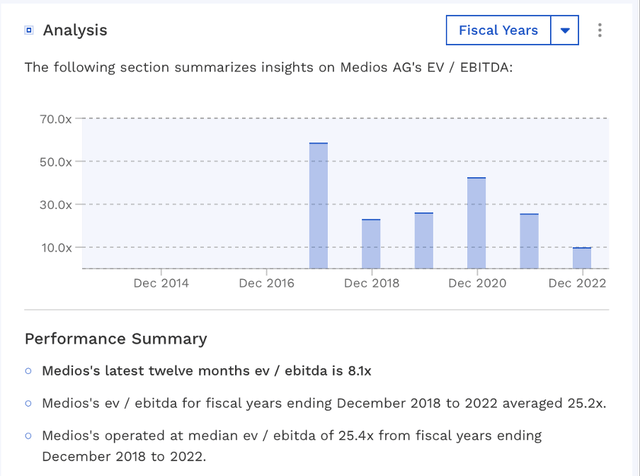

Medios is currently trading at an attractive valuation, with an EV/EBITDA of 8.1x, which represents a substantial discount compared to its historical average of 25x over the past five years. Furthermore, the company is trading at a slight discount compared to its peers.

FinBox

FinBox

As a result, we expect Medios to achieve an EBITDA margin of 3.5% (implying a 100bp increase compared to the 5-year average) over the next five years, while the market is projected to grow organically at 9%. We conservatively estimate that Medios will grow at a rate of 6%, resulting in revenues of EUR 2.2 billion and an EBITDA of EUR 80 million by 2027.

What will be our exit multiple in 5 years?

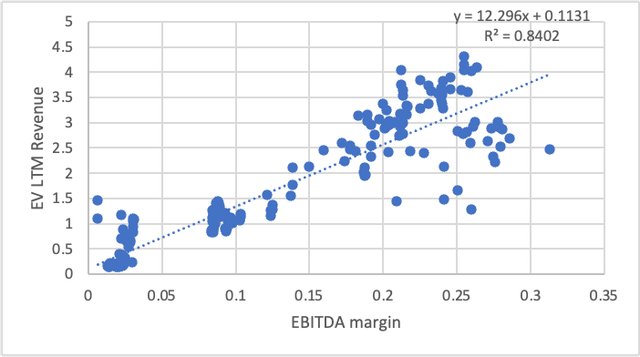

Based on our analysis, we have observed that similar businesses (Drug distributors) with a 3.5% EBITDA margin have been valued at around 0.5x EV/Sales in the last 10 years.

Author’s work – Data: FinBox

Assuming no expansion in the EBITDA margin, the exit EV would be approximately EUR 1.1 billion, resulting in an upside of 175% or an annual IRR of 25%.

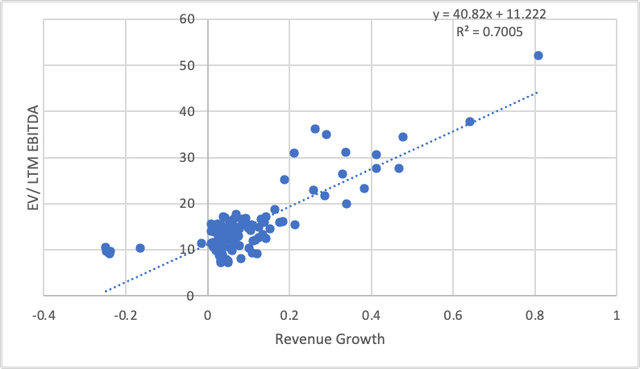

Same conclusion if we take into consideration the growth.

Author’s work – Data: FinBox

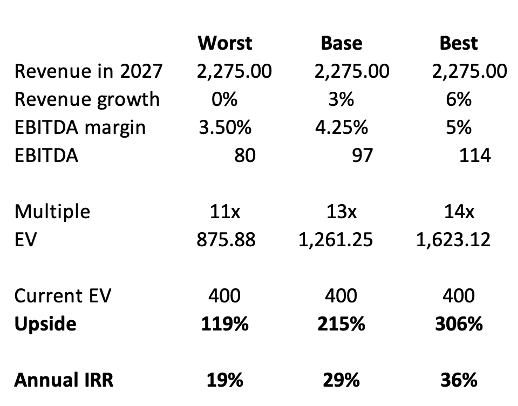

Historically, these companies traded at 11x EV/EBITDA with 0% growth, implying an exit multiple EV of EUR 875 million or an annual IRR of 19%.

However, if Medios can increase its patient-specific therapies to achieve a mid-single-digit EBITDA margin of 5%, we estimate an EBITDA of EUR 114 million, which is likely to result in a significant change in the potential upside.

Author’s Analysis

We believe that Medios is undervalued, as the risk of regulation is already priced into the share price. We do not anticipate any new adjustments or taxes in the near future due to the tight market conditions.

Despite the current unappealing results, we believe that Medios represents a compelling investment opportunity in today’s uncertain times. This is due to the inelasticity of demand for its product, which provides a stable revenue stream even in challenging economic conditions. Additionally, we expect the long-term growth in demand for the product, driven by an aging population, to provide a significant tailwind for the company’s future growth prospects.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

No Byline Policy

Editorial Guidelines

Corrections Policy

Source